In this article, we will share with you the general rules for the application of value-added tax (VAT) in the EU. There may be exceptions to these general rules, which will not be fully disclosed in this article. Additionally, the specific features of VAT application and administration in individual countries will not be described in detail. Each EU member state has its own particularities regarding VAT taxation. For this reason, we strongly recommend seeking advice from professionals practicing in this area.

A bit of history:

In the mid-20th century, the growth of the international market prompted countries to create a tax that would be a reliable source of budget replenishment and stimulate the export of goods. As a result of extensive research, in 1954, French economist Maurice Lauré first described the mechanism of a tax that we now know as value-added tax (VAT). The first place where it was implemented was the then-French overseas territory, now an independent country — Côte d'Ivoire. The results of the experiment were deemed successful, and France officially introduced VAT in the same year, 1954.

Later, other EU countries began to implement VAT. Within the framework of the European Economic Community (EEC), it was introduced in the 1970s in accordance with Council Directive 77/388/EEC (the Sixth Directive). This directive became the foundation for harmonizing the VAT system in Europe.

What is VAT?

(VAT, or Value Added Tax)

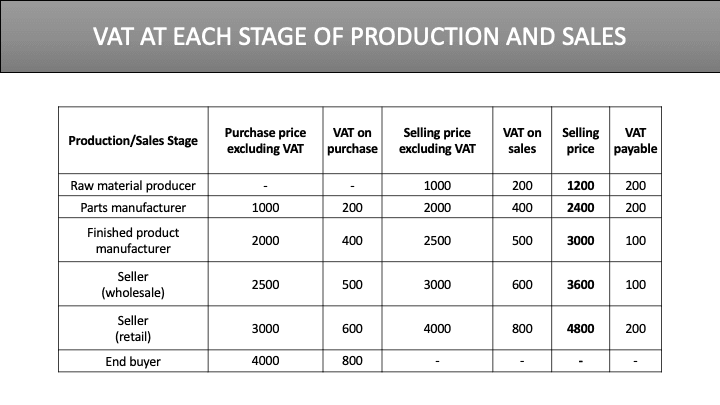

The creation of a specific product or service usually occurs in several stages. At each stage of production, up to the point of sale to the final consumer, the value of the product or service increases (for example, wood purchased for 10 EUR / sold as planks for 15 EUR).

VAT is an indirect tax on the added value that arises during the production and sale of goods or services. All participants in the process, except the final consumer, include VAT in the sale price. As a result, the cost of the product or service increases, and the final consumer pays the full price, which includes VAT.

However, the actual payment of VAT to the budget occurs at each stage of the production and sales chain.

How does this work at the level of a specific company?

When a company issues an invoice to a customer, it adds VAT (sales VAT) to the price. The amount of VAT collected from customers during the reporting period is the company's tax liability to the state and must be paid to the budget.

When the company pays for goods or services from a supplier, it also pays the included VAT (input VAT). The total amount of VAT paid by the company during the reporting period is called the tax credit. The company has the right to deduct this amount from its tax liability to the state, paying only the difference between the VAT collected from sales and the VAT paid to suppliers.

Simple example:

Company X buys fuel briquettes from a supplier for 120 euros (product cost = 100 euros + 20 euros VAT). In this case, 20 euros is the tax credit for Company X.

Then, Company X resells the product to the final consumer for 240 euros (product cost = 200 euros + 40 euros VAT). In this case, 40 euros is the VAT liability of Company X.

Thus, Company X is required to pay the budget the difference between the VAT liabilities and the tax credit, that is: 40 – 20 = 20 euros.

VAT on exports:

As we recall from the history of this tax, one of its main goals was to stimulate exports. Therefore, the export of goods is taxed at a zero rate. The exporter issues an invoice to the buyer without VAT.

A logical question arises: what happens to the accumulated tax credit during production? In this case, the exporter is entitled to a refund of VAT paid at previous stages of production from the budget. However, such a refund is only possible if there is proof of the actual export of the goods outside the country, such as customs declarations, shipping documents, contracts, invoices, etc.

VAT on imports:

Imported goods are subject to VAT to prevent the creation of unfair competitive advantages for foreign suppliers compared to domestic producers. Otherwise, domestic goods would be more expensive, demand for them would decrease, which could lead to a reduction in their production.

In this case, the VAT payer is the importing company, which, after paying the tax, receives the corresponding document (for example, an import customs declaration). This document grants the right to a further tax credit, that is, the possibility to deduct the VAT paid on imports from the total VAT liability.

VAT in the European Union

The unique VAT application rules in each EU country significantly complicated the movement of goods within the Eurozone. This is why the EU member states implemented unified VAT taxation principles based on EU directives. However, in practice, each country has certain exceptions and specificities in applying the tax.

VAT payers are individuals and companies engaged in entrepreneurial activity.

VAT registration in the EU may be voluntary or mandatory (if the turnover threshold established by law is exceeded). After receiving a VAT number, the taxpayer is required to maintain records and regularly submit VAT returns.

Below are the main principles and concepts related to European VAT.

Four main types of transactions subject to VAT in the EU:

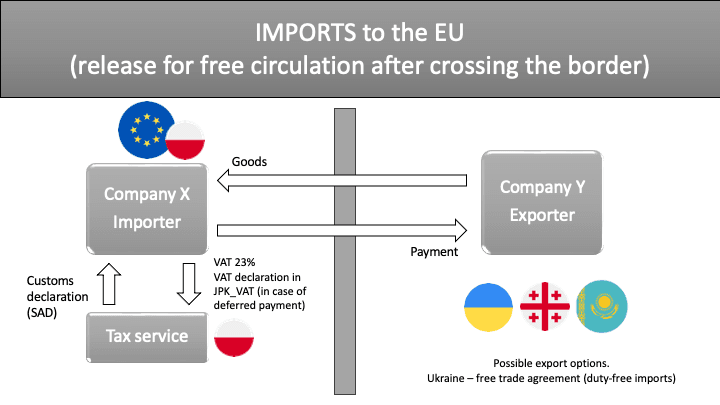

1. Import/Export of Goods

When importing goods into the EU, the importer pays VAT. The rate will be the same as for a similar product produced in the country of import. After paying VAT, the tax authority issues a certificate to the importer, granting the right to reclaim the paid tax.

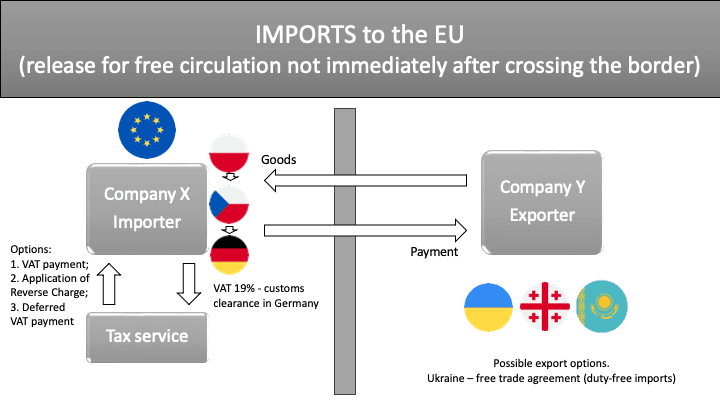

If the goods do not enter free circulation immediately after crossing the European Union border and are moved to another EU country, VAT is paid at the rate of the country where the goods enter free circulation from the special customs regime.

The VAT rate on the export of goods from the EU is 0%. The exporter issues an invoice without VAT but must collect documents proving the export of the goods (customs declarations, shipping documents, contracts, invoices, etc.) to be eligible for a refund of the tax paid on the purchase or production of the goods.

In some EU countries, there is a VAT Deferment mechanism for imports, which allows companies not to pay VAT at customs but instead declare it in their tax reporting and immediately deduct it as a tax credit.

Main countries where VAT deferment is available:

- Netherlands (Article 23 VAT Deferment) – importers can avoid paying VAT at customs, improving cash flow;

- Belgium, France, Germany, Sweden – also have similar programs.

Who benefits from this?

- Companies that regularly import goods to the EU;

- Businesses that want to avoid additional pressure on working capital.

To take advantage of this scheme, the company must obtain special authorization from the tax authorities of the respective country.

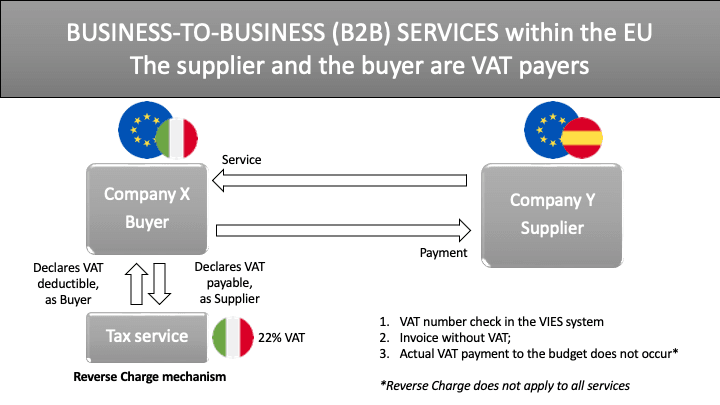

2. Provision of Services B2B (Business-to-Business)

The main principle: Value-added tax arises at the place of service provision, which is usually the place of registration of the buyer.

Mandatory condition: The buyer must provide the supplier with their VAT number (if they are an EU resident) or documents proving that their activity is subject to taxation (if the buyer is a non-EU resident).

IMPORTANT: VAT is not included in the service cost, meaning the supplier issues the invoice without it.

Why is the invoice without VAT?

In this case, the Reverse Charge mechanism applies. This means that the buyer self-declares and pays VAT for both themselves and the supplier. At the same time, the amount of VAT to be paid and the amount of the tax credit usually match, so the tax is not actually paid but only reflected in the reporting.

Starting from 2025, the EU will implement the Digital Reporting Requirements (DRR) system, which involves the electronic recording of transactions in real-time or near-real-time.

However, the implementation of these requirements will be phased in:

- The first countries to implement DRR will be Italy, France, Germany, Poland, and Spain.

- The remaining EU countries will receive a transitional period and will be required to gradually integrate these requirements into their national legislation.

What does this mean for businesses?

- Companies operating in the EU will be required to submit electronic transaction reports to tax authorities in near real-time;

- This will reduce opportunities for tax evasion and VAT fraud;

- Companies outside the EU doing business in Europe will also have to comply with the new requirements, especially when providing services or selling goods through marketplaces.

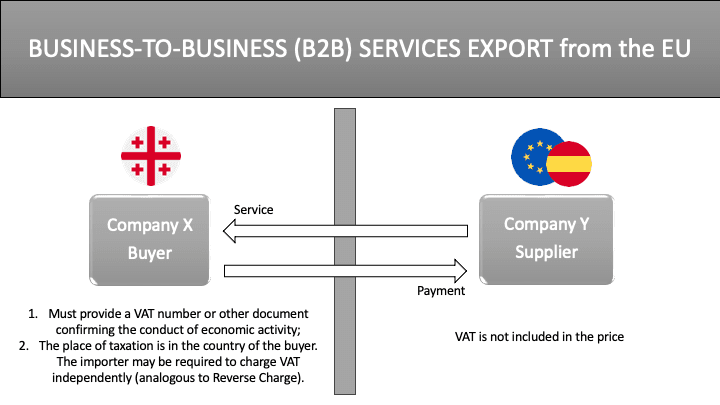

If a European company provides B2B services to a non-EU company (for example, a Georgian company), the supplier must verify documents confirming that the buyer pays corporate tax (profit tax) in their country (for example, in Georgia). After this, the supplier is entitled to issue an invoice without VAT.

There are exceptions to this rule for certain types of businesses. Therefore, it is advisable to consult on the specific case before proceeding with the transaction.

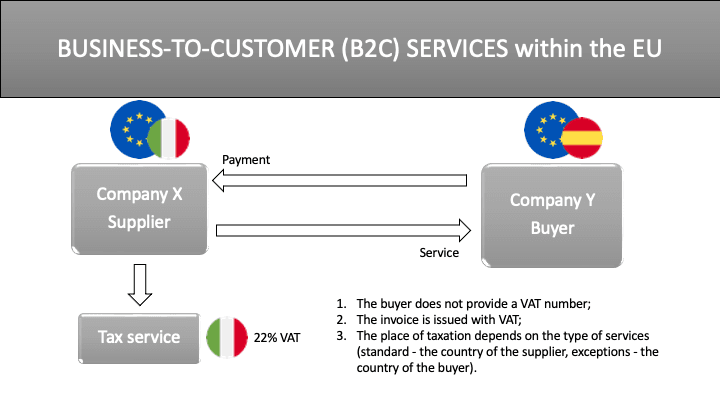

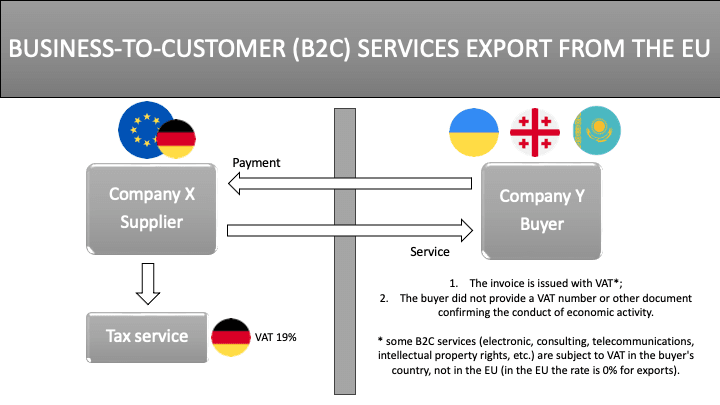

B2C (Business-to-Customer)

The main principle: Value-added tax arises in the country of the supplier.

Mandatory condition: The buyer does not have or has not provided a VAT number (if they are an EU resident) or documents proving their status as a corporate tax payer (if they are a non-EU resident).

This rule mainly applies to services provided to final consumers — individuals.

IMPORTANT: VAT is included in the service cost, meaning the supplier issues the invoice with VAT. Then, they declare and pay the value-added tax.

As with B2B transactions, there are also exceptions to the general rules in this case.

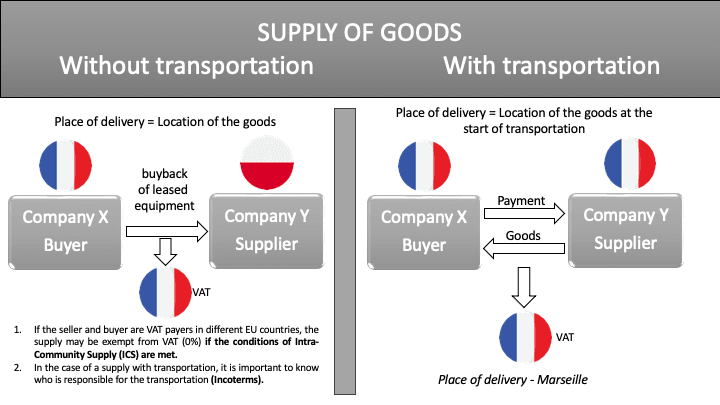

3. Supply of Goods

The main principle: Value-added tax arises at the place of supply.

How is the place of supply determined?

- If the goods are not transported, the place of supply is the location of the goods at the time of sale.

- If the goods are transported, the place of supply is the location of the goods at the start of transportation.

Exceptions: Some situations, such as the supply of goods during passenger transport, may have a special taxation procedure.

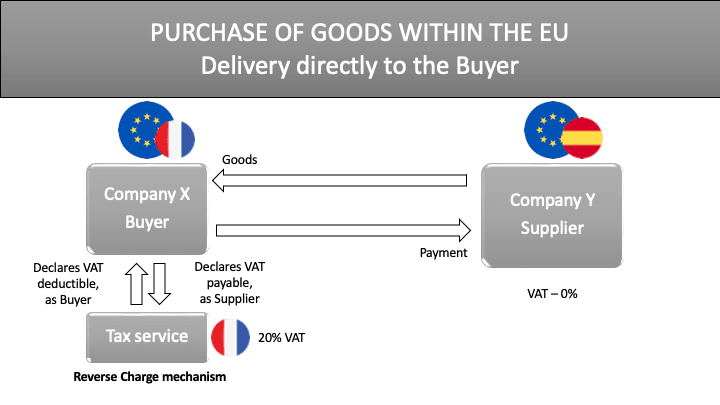

4. Acquisition of Goods within the European Union

The main principle: Value-added tax arises in the country where the buyer acquires the goods (i.e., in the country of actual supply).

IMPORTANT: VAT is not included in the price of the goods, and the VAT rate in the seller's country is 0%.

What does the seller need to calculate the paid VAT?

- Obtain the buyer's VAT number and include it on the invoice.

- Provide tax documents confirming the export of the goods from the country.

If the goods did not leave the country within 90 days or if there are no documents confirming their export, the seller must charge and pay VAT at the full rate.

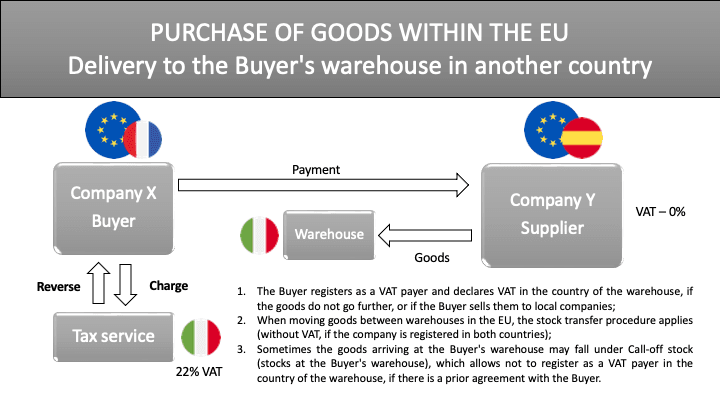

What if the goods are delivered not to the buyer's country of registration, but to a warehouse in another EU country?

In this case, value-added tax arises in the country where the warehouse is physically located. The buyer must obtain a VAT number in that country. The tax is then applied using the Reverse Charge mechanism (as in B2B services).

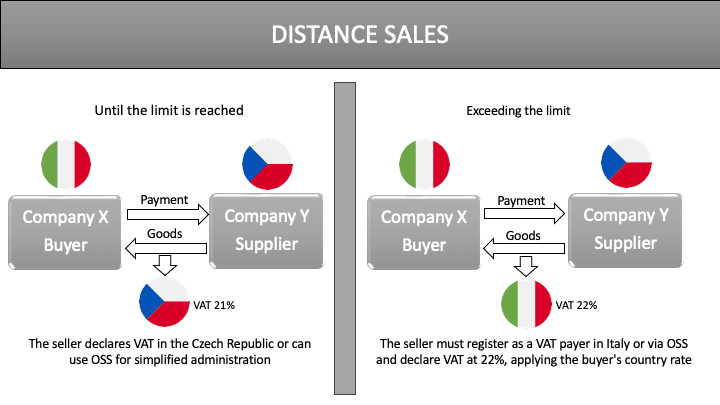

Distance Sales and New Rules for Marketplaces

Distance sales refer to sales to final consumers (B2C). Final consumers are buyers who are not VAT payers or have not provided their VAT number.

Changes in the rules from July 1, 2021:

Previously, each country set an annual threshold for distance sales (for example, in Estonia – 40,000 EUR). If this threshold was exceeded, the seller had to register in the buyer's country and pay VAT there.

New rules:

- A unified threshold of 10,000 EUR for all distance sales within the EU has been introduced;

- Until the 10,000 EUR threshold is reached, the seller may apply the VAT rate of their own country;

- If the total turnover of distance sales within the EU exceeds 10,000 EUR, the seller must charge VAT at the rate of the buyer's country;

- The seller can choose one of two options for administering VAT:

- Registering as a VAT payer in each country where sales occur.

- Using the One Stop Shop (OSS) – a single reporting window.

If the distance sale involves digital products (e-books, online courses, software, subscriptions), they are always taxed at the VAT rate of the buyer's country, regardless of turnover.

What are One Stop Shop (OSS) and Import One Stop Shop (IOSS)?

The EU has introduced two special schemes to simplify reporting:

- OSS (One Stop Shop) – an online portal for reporting B2C sales within the EU. It allows sellers to avoid multiple VAT registrations in the buyer's countries and submit a single quarterly report with VAT payments in one country.

- IOSS (Import One Stop Shop) – a scheme for importing goods worth up to 150 euros. It allows sellers to charge VAT immediately at the point of sale and report it in a monthly return.

Starting from 2025, there will be some changes for marketplaces:

- Marketplaces (Amazon, eBay, Etsy) will have expanded responsibility for paying VAT if the seller is outside the EU or the goods cost up to 150 euros.

- Tax authorities in EU countries will gain automatic access to information about sales made through marketplaces.

How does this work?

- If the seller is not an EU resident and their product costs up to 150 euros, the marketplace will collect VAT at the point of sale;

- All major marketplaces will be required to provide tax authorities with data on sales, allowing better monitoring of compliance with the rules.

What does this mean for businesses?

Companies outside the EU will need to adapt to new reporting rules as the EU actively combats VAT evasion in the e-commerce sector.

Buyers can expect greater transparency and fewer "hidden" taxes when purchasing goods through international online platforms.

Platforms providing services or selling goods within the EU will bear greater responsibility for properly accounting for VAT. They will be required to provide tax authorities with detailed information about transactions conducted through their systems.

Triangular Transactions

What is triangulation?

A triangulation agreement is a simplified VAT procedure for trade between three companies registered in different EU countries. It allows the intermediary (Company Y) to avoid the need to register in the seller's or buyer's country.

Example of the agreement:

Company X (Seller, Country A) → sells goods to Company Y (Intermediary, Country B);

Company Y (Intermediary, Country B) → resells goods to Company Z (Buyer, Country C);

The goods are shipped directly from Country A to Country C.

How VAT works:

- Company Y (the intermediary) does not need to register for VAT in countries A and C.

- They must provide the VAT number of Country B to the seller.

- The seller (X) issues the invoice at a 0% rate according to EU rules.

- Company Y also issues an invoice to Company Z without VAT, but with a note about the triangulation agreement.

- Company Z self-declares VAT in its country (C).

Advantages of triangulation:

- The intermediary (Y) does not need to register for VAT in other countries;

- It reduces administrative costs;

- It allows for faster transactions between different jurisdictions.

VAT rules for small and medium-sized enterprises (SMEs) in the EU

Starting January 1, 2025, small businesses in the EU will be able to benefit from VAT exemption not only in their country of registration but also in other EU countries, provided their annual turnover does not exceed:

- 85 000 euros in the country of registration (or a lower threshold set by national legislation);

- 100 000 euros for companies operating in several EU countries.

What will change?

- Previously, companies had to register for VAT in each country where they made sales, but now they can use a simplified taxation system;

- Small businesses can reduce administrative burden and avoid adding VAT to the cost of their goods/services, improving competitiveness.

How to benefit from the simplified system?

The company must apply for the special VAT regime in its country of registration. It is also required to maintain accounting records and submit relevant reports, even if exempt from VAT.

If the threshold is exceeded, the company will need to register for VAT in the countries where sales occur. However, using the One-Stop-Shop (OSS) system simplifies the process of filing returns and paying tax, providing a single point for VAT administration in all EU countries.

Need help with VAT registration or administration in the EU? If you have any questions, feel free to reach out for advice! We analyze each case individually and collaborate with experienced European accountants to offer optimal solutions for VAT registration and administration.

Sources:

- EU Council Directive 2006/112/EC of November 28, 2006;

- EU Council Directive 2008/8/EC of February 12, 2008;

- EU Council Directive 2008/9/EC of February 12, 2008;

- EU Council Regulation No. 143/2008 of February 12, 2008;

- European Commission Regulation (EC) No. 282/2011;

- European Commission Report on the adaptation of the digital economy to new VAT rules;

- EU Council Regulation (EC) No. 904/2010 on administrative cooperation in VAT.

Written by: Oksana Kolobanko. Head of Finance Department, Taxters. February 2025