In this article, we will review the general rules for applying VAT (Value Added Tax) when providing electronic services in the EU. Please note that possible exceptions to the general rules presented will not be fully covered. It is also important to consider that, starting in 2025, additional VAT administration rules have been introduced in the EU, particularly within the OSS system, which may impact the reporting obligations of electronic service providers.

The OSS system applies not only to electronic services but also to the remote sale of goods and other B2C services within the EU. This is crucial for companies supplying goods to end consumers who wish to avoid registering separately in each country.

Additionally, since 2023, European financial institutions have been monitoring transactions related to the purchase of digital services and Ecommerce sellers to ensure mandatory VAT registration. The CESOP (The Central Electronic System of Payment Information) has been introduced and is currently in operation.

What Are Electronic Services?

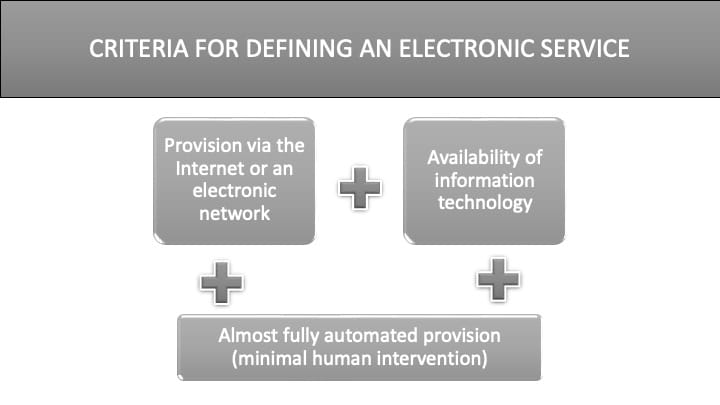

Electronic services, also known as services provided through electronic communication channels (ESS - electronically supplied services), are services that:

- are delivered via the Internet or an electronic network;

- are predominantly supplied in an automated manner (requiring little to no human intervention);

cannot be provided without the use of information technology.

Examples of Electronic Services

- Supply of digitized products, including software, modifications, and/or updates;

- Web hosting services;

- Automated support and technical maintenance of web resources;

- Online data storage, where certain data is stored and retrieved electronically;

- Installation drivers, such as software that connects computers to peripheral devices (e.g., printers);

- Online access to or downloads of photos, movies, music, games, and books;

- Provision of advertising space, including banner ads on websites/web pages.

How to Determine if a Service is Electronic?

To classify a service as electronic, it should be checked against:

- The lists defined by the EU VAT Directive or the Implementing Regulation regarding its application;

- If not listed, the list of services that do not fall under the definition of electronic services, found in Article 7(1), paragraph 3 of the Implementing Regulation;

- If the service is not included in either list, it should be assessed against the general definition of electronic services outlined above.

Who and Where Should Pay VAT?

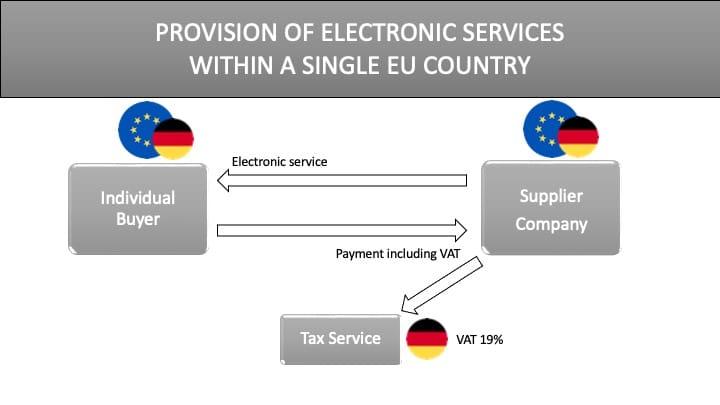

Since January 1, 2015, electronic services are taxed in the buyer's country, regardless of whether the buyer is a legal entity or an individual.

Important! If the total annual turnover from remote sales of goods and electronic services to end consumers in the EU does not exceed €10,000, the company may continue applying the VAT rate of its country of registration. However, if this threshold is exceeded, the company must register in the One Stop Shop (OSS) system and pay VAT in the buyers' countries.

This threshold applies only to companies registered in the EU. Non-EU companies must register in OSS regardless of their sales volume.

Important! The rule of taxation in the buyer's country does not apply to the supply of physical goods, even if electronic systems are used solely for order placement.

If the following conditions are met simultaneously:

- Your European company provides electronic services to a client from another EU country;

- The client from another EU country is not a VAT payer or has not provided you with their VAT number;

- Your company's services are provided directly to the client, not through a marketplace.

then your company must issue an invoice to the client, including VAT at the rate of the client’s country. After that, the company must report this VAT either directly in the client’s country or in its own country through the simplified VAT administration system – OSS (One Stop Shop).

If at least one of these conditions is not met, the consequences will differ.

More details on these scenarios can be found below.

If your company has clients only in the country of registration, it must report and pay VAT only in that country (provided that the company is already registered or is required to register as a VAT payer after reaching the domestic turnover threshold).

If your company has a client from another EU country who is a VAT payer (i.e., they have provided their VAT number), then they report VAT in their own country independently under the reverse charge mechanism.

If your company provides electronic services through a marketplace, this is considered the provision of services to a VAT-liable entity (i.e., the marketplace operator). The marketplace operator, in turn, supplies the service to the final consumer, who is not a VAT payer. In this case, the marketplace operator is responsible for VAT reporting and payment in the country of registration or the location of the final consumer.

IMPORTANT: If a company is not registered as a VAT payer in its own country but provides electronic services to EU residents, it must either register in OSS or become a VAT payer in each country where it has clients.

How to Determine Your Client’s Location?

There are two general rules for identifying the customer’s location.

If the client is a legal entity (a taxpayer who has provided their VAT number), their location is considered to be either the country of registration or the country where they have a permanent establishment (e.g., a warehouse, production facility, etc.) in relation to which they receive the service.

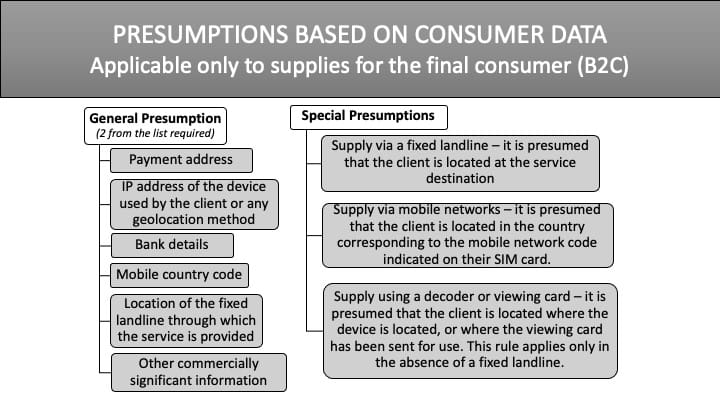

If the client is an individual – a final consumer, their location is determined based on the following criteria:

- The buyer’s country of registration;

- Their permanent address;

- Other factors confirming their place of residence (e.g., IP address, banking details, mobile operator SIM card).

In practice, determining a client’s location can be challenging, especially if such data is not required for accessing the electronic service.

In such cases, EU legislation provides a set of presumptions to simplify VAT application. This means you can determine the client’s location based on the available data. In 2025, an expansion of the criteria is expected to provide clearer guidelines.

The general presumption applies when it is not possible to use specific presumptions. It allows the determination of the client’s location based on two points, provided that the information from one point does not contradict the other.

There are also presumptions that do not fall under the general rule, such as those applied to the supply of electronic services on board a means of transport.

What if the specific and general presumptions indicate different client locations? You may (but are not required to) override the specific presumption if you have three independent pieces of evidence from the general presumption. Tax authorities can override presumptions only if they detect signs of abuse by the supplier.

Fulfilling VAT Obligations

There are two main ways to comply with VAT obligations:

- Registering for VAT accounting and payment in each EU country where your clients are located

- Registering through the One Stop Shop (OSS) system, which simplifies VAT reporting for companies supplying goods and services to end consumers within the EU.

The first method is impractical if your company has clients in more than two countries and plans to expand into additional markets. Therefore, we will focus on the second option, which offers more opportunities and involves less bureaucracy.

Since July 1, 2021, the VAT MOSS (Mini One Stop Shop) system is no longer in use. It has been replaced by the One Stop Shop (OSS) system.

OSS is a system that allows companies to submit a single VAT return and pay VAT on all sales of goods and services to final consumers across the EU through a single country of registration. This simplifies VAT administration for companies with clients in multiple EU countries.

The €10,000 registration threshold applies to the total distance sales across the EU, not separately for each country. This means small businesses can avoid OSS registration if their total sales to final consumers in the EU remain below this threshold. However, if this limit is exceeded, the company must apply the VAT rates of the buyers' respective countries.

OSS System has three schemes:

- Union OSS - applies to companies registered/having a head office/at least one branch in the EU;

- Non-Union OSS - applies to companies with no branches in the EU but providing services to EU residents.

- Import One Stop Shop (IOSS) – a special scheme for importing goods valued up to €150 for final consumers in the EU. It allows suppliers to declare and pay VAT on imported goods through a single country of registration, simplifying import processing.

Starting in 2025, automatic verification mechanisms for OSS registration will be introduced through the European tax database. EU tax authorities will be authorized to automatically check companies with significant sales volumes in the EU that have not registered for OSS.

When Should the OSS Return Be Submitted?

Until 2025, the OSS return had to be submitted within 20 days after the end of the quarter. Starting in 2025, the submission deadline has been extended to 30 days after the end of the quarter.

What Should Be Included in the OSS Return?

The return must include: total turnover (excluding VAT), applicable VAT rates, total VAT amount collected from customers, broken down by the countries where the supplies were made.

Before submitting the return, it is advisable to check the latest VAT rates in EU countries on the European Commission’s website.

When Should the Declared VAT Be Paid?

The VAT amount specified in the return must be paid no later than the last day of the month following the end of the reporting quarter.

If the payment is not made on time, the company may face penalties or be temporarily excluded from the OSS system.

| Company | |||

| Established in the EU / Has a Head Office in the EU | Has a Branch in the EU | Established Outside the EU and Has No Branches in the EU | |

| Application of the Scheme | Can Be Used for Providing Services to Buyers from All EU Countries, Except:

| Can Be Used for VAT Reporting on All Supplies of Goods and Services to Final Consumers in the EU | |

| Choosing the OSS Registration Country | Company's Country of Registration or Location of Head Office | Any EU Country Where a Branch Is Located | Any Chosen EU Country (Under the Union OSS or Non-Union OSS Schemes). If a company uses the Import One Stop Shop (IOSS) for importing goods valued up to €150, it must select a registration country where VAT on imports will be administered. |

| Registration | Online procedure | ||

| Registration Activation | If not stated otherwise, registration will begin on the first day of the calendar quarter following the company’s notification to the tax authority about joining the scheme. | ||

| Preliminary activation of Registration | A company may request to join the scheme before the start of the next quarter. It must notify the tax authority by the 10th day of the month following the first provision of relevant services. | ||

| If the Service Was Provided but the Company Is Not Registered in OSS | A company must inform the OSS registration country's tax authority by the 10th day of the following month that it has made such a supply. In this case, the registration will take effect from the date of that supply. | ||

| Deregistration | If a company decides to cancel its registration in the scheme, it must notify the tax authority of the OSS registration country at least 15 days before the end of the calendar quarter. Once the request is accepted, the company will receive an electronic confirmation and will not be able to use the scheme again for six months. | ||

| Exceptions to the Scheme | Starting in 2025, the European Commission plans to tighten control over companies that systematically violate OSS rules. Companies that fail to submit reports twice in a row will be temporarily excluded from the system. A Company Loses the Right to Use OSS If:

Minimum Violation Criteria A company may be excluded from OSS if:

| ||

| Temporary Exclusion (Quarantine) | If a company violates OSS reporting rules (e.g., fails to submit declarations or incorrectly determines the place of supply), it may be excluded from the system for 2 years. If the company corrects the violation but has already been excluded, it can reapply for registration no earlier than 12 months later. | ||

| VAT Taxation Rules |

|

| |

| VAT Return | · Until 2025, the OSS return had to be submitted within 20 days after the end of the quarter. From 2025, this deadline has been extended to 30 days after the end of the quarter; · Tax authorities in the registration country forward the information to other EU countries; · In addition to OSS, the company must submit a regular VAT return in its country of registration. | ||

| Record-Keeping | The company must retain records of the services provided for at least 10 years in a format accessible to the tax authorities of any EU country upon request. Tax authorities may request this data within this period, even after the company exits OSS. The information must be available to tax authorities without delay. Recorded Data Includes: · Consumer’s country where the service is provided; · Type of service provided; · Date of supply of the service; · Any subsequent increase or decrease in the taxable amount; · Applicable VAT rate; · VAT amount payable, specifying the currency used; · Dates and amounts of received payments; · Any advance payments received before the service supply; · If an invoice was issued – information contained in the invoice; · Client’s name/company name, if known to the taxpayer; · Information used to determine the client’s place of registration/permanent address/usual place of residence. | ||

EU VAT Rules Are Constantly Evolving and in 2025 businesses will need to pay even closer attention to registration, reporting, and VAT payment. To avoid penalties and simplify VAT administration, it is advisable to prepare in advance for the new requirements.

💡 Need to know whether your company must register for OSS, where, and how to declare VAT to save time and minimize risks? Leave a request for a consultation, and we will help you navigate all the details.

Sources:

- Council Directive 2006/112/EC of 28 November 2006 on the common system of value added tax;

- Council Implementing Regulation (EU) No 282/2011 of 15 March 2011 laying down implementing measures for Directive 2006/112/EC on the common system of value added tax;

- Publications on the European Commission's Website:

- Proposal for a Council Directive amending Directive 2006/112/EC as regards VAT rules for the digital age (ViDA), European Commission, 2022.

Written by: Oksana Kolobanko. Head of Finance Department, Taxters. February 2025